CPF: 3 ways to avoid spending your golden years in “survival mode”

In recent years, there have been many articles of old folks in Singapore living in poverty. This prompted Dr Alexandre Kalache, former head of ageing issues at the World Health Organization (WHO) to voice concerns that Singapore still has much room for improvement in terms of helping elderly to age with dignity. Whilst I do not have the data to illustrate the profile and root causes leading to the plight of these people, at the back of my mind, I wonder to myself what it is like to spend my golden years in survival mode. Can CPF savings be your ticket to retirement?

Perhaps one of the most controversial topics among Singaporeans would be – Do you really need your CPF to retire? Is the CPF scheme still effective in addressing the retirement needs of Singaporeans? To tackle these questions, one needs to trace the history of CPF and its original intent.

Implemented in 1955, CPF is a compulsory savings scheme that requires all employers and employees to contribute a portion of the employee’s monthly gross salary to their CPF fund. In those days, most workers depend solely on their personal savings when they retire and most employers did not provide any form of retirement benefits to their employers. So the government deemed that a provident fund was necessary to ensure that Singaporean workers can support themselves in their retirement age.

Since then, CPF has undergone significant changes over the years with the introduction of the Special Account in 1977 and the Medisave Account in 1984, as well as the usage of CPF funds for investment and education purposes. You can even use your CPF Ordinary Account to buy property. The changes made to CPF are part of an evolution to cater to the growing aspirations and changing needs of Singaporeans.. To achieve financial freedom in retirement, one really needs to have the correct mindset when it comes to CPF and retirement funds.

Engage in more than one channel of passive income

Firstly, it is not wise to build your retirement nest egg solely on CPF savings. Although the CPF system is a scheme designed by the government to provide basic retirement needs for Singaporeans, the framework is never meant to be customised to different needs. As everyone has different lifestyle needs, expenses and saving habits, to rely solely on your CPF to retire may not be a wise choice. Therefore, at the very beginning, you should tell yourself that CPF is only a supplement to your basic needs. Ultimately, the onus is on oneself to build wealth through developing various streams of passive income to support one’s needs during old age.

Do your sums early

Deemed as the best social security system in Asia for three consecutive years by Mercer, the CPF scheme allows Singaporeans to use their Ordinary Accounts for housing, to support their children’s tertiary education, to invest, and to cover medical expenses. Such flexibility is always a double-edged sword.

Perhaps a victim of its own success, the wide array of schemes introduced to the CPF system raises the prospect that retirement may not be secure for many Singaporeans. This is because of the possibility of poor investments and excessive use of CPF for housing or education. If you belong to this category, then the prospect of living your golden years in survival mode is very real, especially if you intend to depend solely on your CPF monthly pay-outs after you retire.

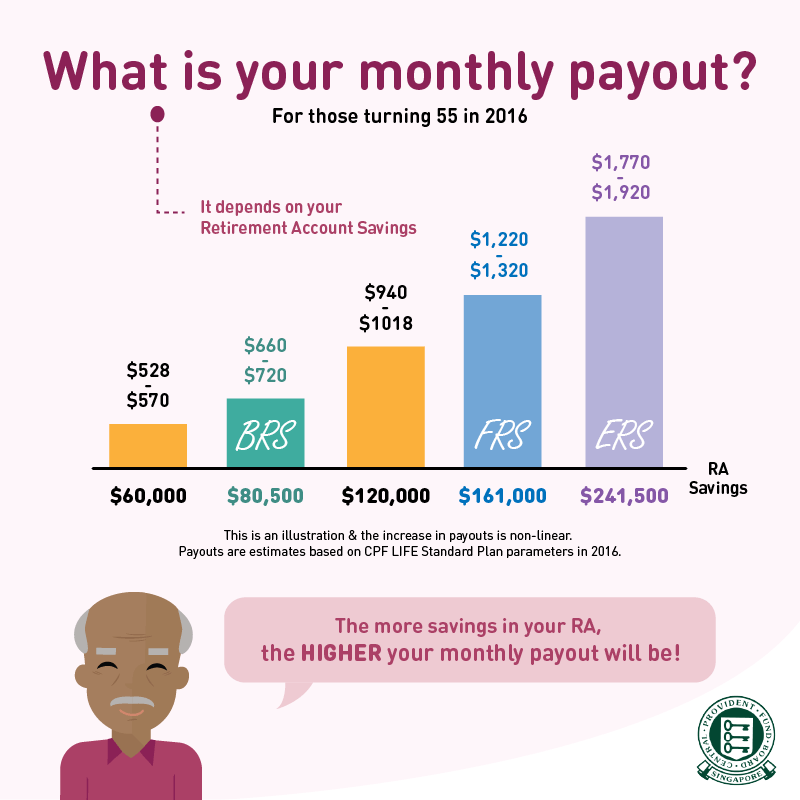

The monthly payouts for life from 65 is only $660 (assuming you have $80,500 in your Retirement Account at the age of 55). Of course, $660 can provide you three simple meals a day but beyond that, nothing more. I have not even touched on the bills and unforeseen healthcare needs that you cannot claim from Medisave.

Thus, it is likely that you will not be able to enjoy life comfortably with your partner without worrying about money.

Most people don’t bother to think about their “survival” expenses, probably because of denial or sheer procrastination. To this end, I would strongly encourage readers to calculate and find out how much it takes to make ends meet for each month. Knowing this would enable you to be more resolute in achieving financial freedom in your retirement age. Personally, my wife and I don’t track our daily living expenses. However, we are responsible enough to calculate our monthly “survival” expenses and to ensure that we do not over-spend.

To prevent the situation of your retirement funds being compromised, you should assess whether you can afford that new house, invest in companies that yield dividends higher than CPF interest rates and think twice whether to use your CPF monies to support your children’s tertiary education (when they can take personal loans). These are complex issues that really need to be well-thought through and not something you should take lightly.

Consider working beyond 65

Fundamentally, as an ageing society, the issue of retirement will force Singaporeans to re-examine priorities and outlooks in their lives. It is important to continue working so as to remain mentally healthy, socially engaged and have extra money for leisure activities. Essentially, in your golden years, you should be transiting from the phase “work to live” to “live to work”. You might be forced to take on second career or jobs that pay much lower in your previous jobs. But with the CPF payouts, coupled with passive incomes from stocks investments, property rental incomes and endowment plans, you should be able to see out your remaining years in comfort.