Property Financing

Like blogger YP, many Singapore investor lost money from dabbling in the property game because their mindsets are not correct. First of all, to win the game, you must discuss with your spouse the key reason for buying a property. This is an all-important issue that must be addressed before you even step into the show-rooms. This is because the factors for “buying-for-living” and “buying-for-investments” purposes are different. Obviously if you are buying the property to live in, there would be emotional attachments involved and the criteria list that you set would be different from the properties which you wish to rent out. Most home-owners mistakenly thought that they could resolve this issue later and just jump straight into the bandwagon. Eventually, when things turn soured, they regretted skipping this first step.Secondly, investors should not assume that everyday is Sunday and should design contingency plans for unexpected events. Property investors should be mindful that unlike shares, bonds and gold bullion, property is very illiquid and capital intensive. Therefore to make money from property, investors must have holding power (in terms of cash flow) and do their due diligence before committing their monies. Do not adopt a herd mentality and enter the market just because your friends or families have done so. Each of us have different financial pathways and what worked for others, might not work for you.

Thirdly, most Singaporeans may overlook the importance of financial planning before buying a second or new property. But in today’s context, I don’t blame them. After all, how many home-owners have a clear understanding of all the cooling measures that the government had implemented over the last three years?

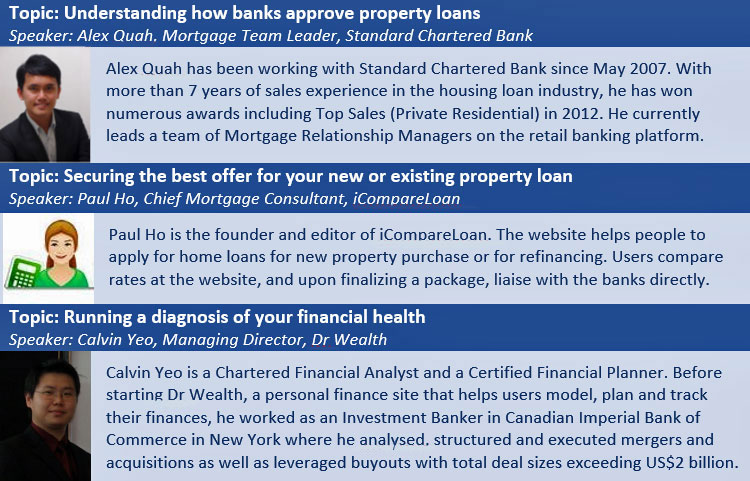

And how many of us are aware of how these measures would impact our property transactions? I bet not many of us would know unless you work in the real estate industry or if you had recently completed a property transaction. To this end, Property Club Singapore is organizing a seminar on property financing and TDSR Framework Education. Home-owners and property investors should grab this opportunity to educate themselves on the process of financing their property. You can register for the seminar through here.

Synopsis

What are the procedures and criteria for banks to approve housing loans?

How can you prove to the banks that you are a good pay master?

What are the common misunderstandings of the TDSR framework?

Which is the best tool for step-by-step calculation of affordability and debt ratio?

How to negotiate with banks for the best deal for your property mortgage?

What advantages can priority banking customers enjoy in their property loans?

How do banks deal with late payments, loan defaults and negative equities?

Seminar details

Date : September 21, 2014 (Sunday)

Time : 2.30 p.m. – 5.00 p.m.

Venue : National Library Building

Agenda

Fee

Member: $35

Non-member: $55

1. Registration fee includes a goodie bag from sponsors.

2. Seats are limited. Registration will be closed once function room reaches full capacity.

Magically yours,

SG Wealth Builder

Discover more from SG Wealth Builder

Subscribe to get the latest posts sent to your email.