July’s Stock Markets Outlook

Guest blogger Argutori is an avid blogger who manage a private portfolio. His fund pursues a fundamental value oriented strategy focusing on developing and frontier markets in the Asian region. The fund focuses on countries that have progressive foreign investment policies, young and growing populations, and stable or improving economic situations. The aim is to find and invest in companies that have stable franchises for good prices before the masses.

While my blog is largely focused on Southeast Asian stock markets, I also try to keep things in perspective and consider the global situation. Stock markets have had a relatively good run so far this year and there is a lot weighing on the US recovery, which has spilled over to emerging markets. I’m struggling to piece together the economic data, media commentary and market movements, which appear to me to be disjointed. Which lead me to ask “What’s really going to happen with equity markets for the rest of this year and how can I best position my portfolio?”

It feels like the world’s gone crazy and the markets aren’t acting in line with rational expectations – worse than anticipated economic data sends the markets up because it means that the Fed will have to keep pumping dollar bills into the system. 44% of 54 economists that Bloomberg surveyed expected the Fed to start trimming back on the amount of bond buying later this year. This could happen but I have a different opinion on why Bernanke made the comments about tapering.

There’s mixed evidence about the improvement in the US

There are a number of charts and economic analysis which paint a dreary picture of the US economy at odds with the perspectives that would lead Bernanke to suggest a reduction in tapering is necessary because of improved underlying conditions. On Wednesday the Bureau of Economic Analysis revised its first quarter GDP growth estimate to +1.8% from +2.4% previously, which was already below expectations of +4.0%, the US economy is stumbling along and job growth isn’t coming through as initially anticipated. The green shoots that economic commentators started talking about in 2011 are still just that.

Annual Changes in Durable Goods Orders

A decline in the velocity of money is traditionally linked to a recession (shown in red), at the moment, the velocity of money isn’t heading in the right direction to suggest that green shoots are becoming a fertile field. The second chart below shows inflation expectations, based on the yield from the 10 year Treasury, which, much to the Fed’s disappointment, are still looking muted.

US Velocity of Money

US Inflation Expectations

To try to kick-start the economy, the Fed has been expanding the monetary base by around 30% a year (some of the purchases are funded with the proceeds from maturing treasuries) but this hasn’t flowed through to ignite inflation in the economy. Why? Most of the newly minted money has been flowing into financial assets and not real or productive assets as the Fed would have hoped. People aren’t buying things and investing in the real assets so the US economy will continue to struggle along below potential GDP until there’s something that causes a change in the market’s mentality.

US Monetary Base – FRED

US Monetary Base

Why did Bernanke hint that the Fed would taper their asset purchases?

In my opinion, there are two reasons that could justify Bernanke’s recent comments:

Firstly, taking the Heroin Addict approach, he’s trying to prepare the market to be able to handle the eventual withdrawal of stimulus. Rather than going cold turkey and turning off the stimulus with the flick of a switch, Bernanke’s attempting to use his comments, much like methadone, to guide the market towards a soft landing.

The ideal outcome in this situation would be for the stock market to take the hint and start to sell off slowly. However, I believe that any reprieve will be short-lived with low rates and volatility driving up the demand for riskier assets. This will cause a rally in stock markets, which leads me to the other potential reason for Bernanke suggesting tapering is just around the corner.

The Frankenstein approach, the Fed is scared that they’ve created an inflationary monster, they need to stop the quantitative stimulus because they’re unsure of what the final impact will be. All he knows is the current impact hasn’t been what he desired or anticipated. The Fed can’t see it and don’t know when it’ll erupt onto the scene but they know it’s there, they know they’ve printed enough money to bring an economy back from the dead. The only problem is… the message hasn’t got through to the economy. The Fed has to start pulling back the amount of quantitative easing because it’s getting to the point that when inflation starts it might be too ravenous and rapid for them to control.

What’s going to happen from here?

We’ve had a flood of money going into financial markets as investors try to make the most of the last days of the long summer. At some point in the near future (maybe the literal end of summer in the Northern hemisphere) we’re going to get to an inflection point where the Fed gets its wish and:

- Hot money gets spooked out of financial markets – Volatility spikes and investors get scared, pulling their money out of financial markets.

- The money will find a new home – The money that has come out of the financial assets will gravitate towards real assets.

- Inflation ramps up quickly – The increase in money moving into real assets will drive up inflation causing a new trend in real assets and inflation hedges.

It’s at this point that inflation hedges will do particularly well, while I’m no gold bug, I believe that there will be another rally in gold as US investors and central banks increase their positions in gold as a hedge against inflation and a rapidly declining US dollar (there are a lot more US dollars out there now).

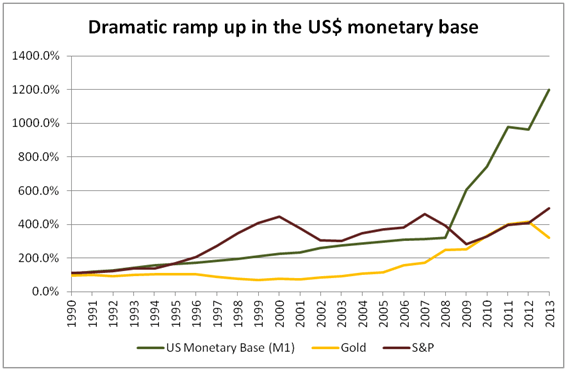

Dramatic ramp up in the US$ monetary base

The chart above scares me, as you can see the supply of money (via printing) has increased dramatically since 1989 but when compared with the price of gold in USD and the S&P500, neither measure has had a corresponding rise. I’d expect the S&P500 to follow a similar trend line but only when the fundamentals justify it. Since there hasn’t been an equivalent amount of inflation in the economy the fundamentals in the stock market are getting out of whack.There is a lot of hot money in the stock market at the moment, which will react as it reaches the reflection point and volatility increases (see El-Erian’s comments about the mechanics of VAR). To avoid the increase in volatility and corresponding sell-off in equity markets, gold will likely re-rate as investors seek to safe-guard the value of the savings against the roaring inflation that will follow.

What am I doing about it?

Buying Gold + Volatility

I believe that as we approach the turning point, volatility will jump and equities will sell-off.

When’s gold’s decline going to stop?

While I don’t spend a lot of time pouring over charts and looking at technical analysis, other people do and as such glimpses into historical levels can give some indication of where we could expect to see a turning point. I acknowledge that it’s difficult to call the bottom and prefer to start purchasing when the fundamentals look appealing and I can envisage a catalyst. It’s difficult in this situation to see a catalyst because of a lot of other investors have got their fingers burnt trying to anticipate gold’s rise but I’ll save that topic for another post. Taking a simple technical analysis approach, there are a few support levels around the current price (US$1,200) and then further down at US$1,000. Since I can’t pick the bottom I’m going to begin building a position from here.

Gold – Technical Analysis

Disclosure: As at writing, I am long gold. If you’re considering investing, please do your own due diligence.

Discover more from SG Wealth Builder

Subscribe to get the latest posts sent to your email.